I have taken this explanation from Microsoft docs page and later part tried to create these scenarios in D365 see how actual transaction looks.

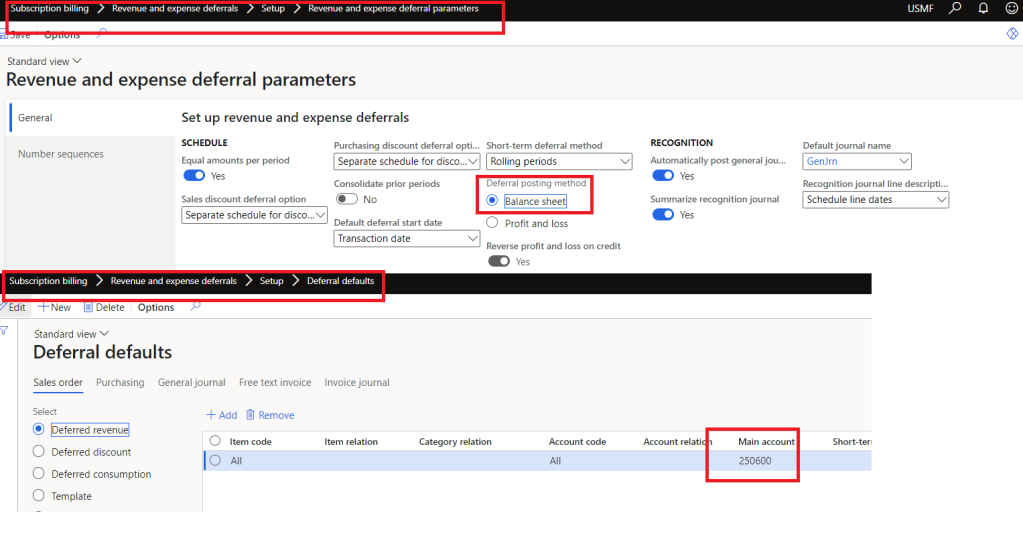

On the Revenue and expense deferral parameters page, the options for deferral posting methods are Balance sheet and Profit and loss. The example in this article will help explain the differences between the two methods and the reasons why you might use one method or the other.

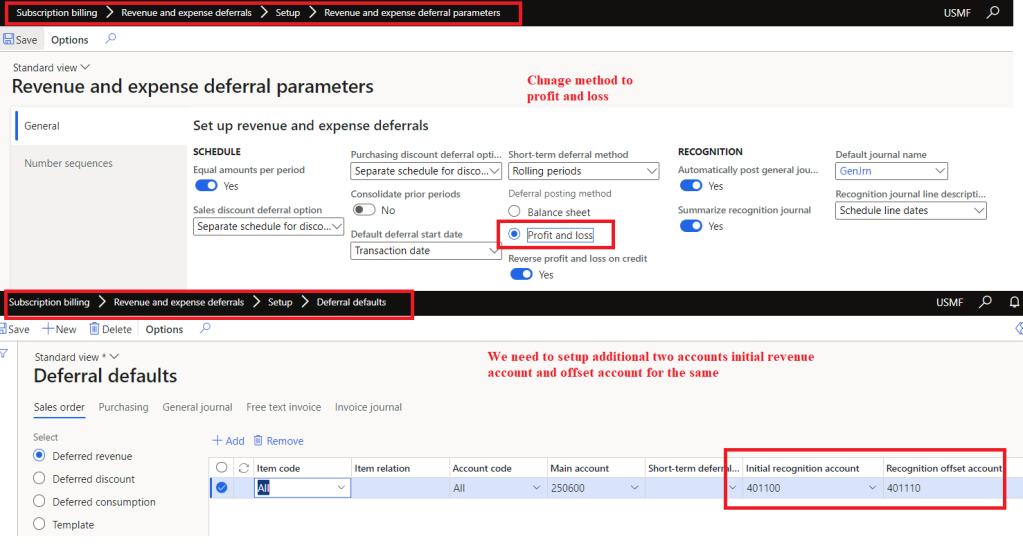

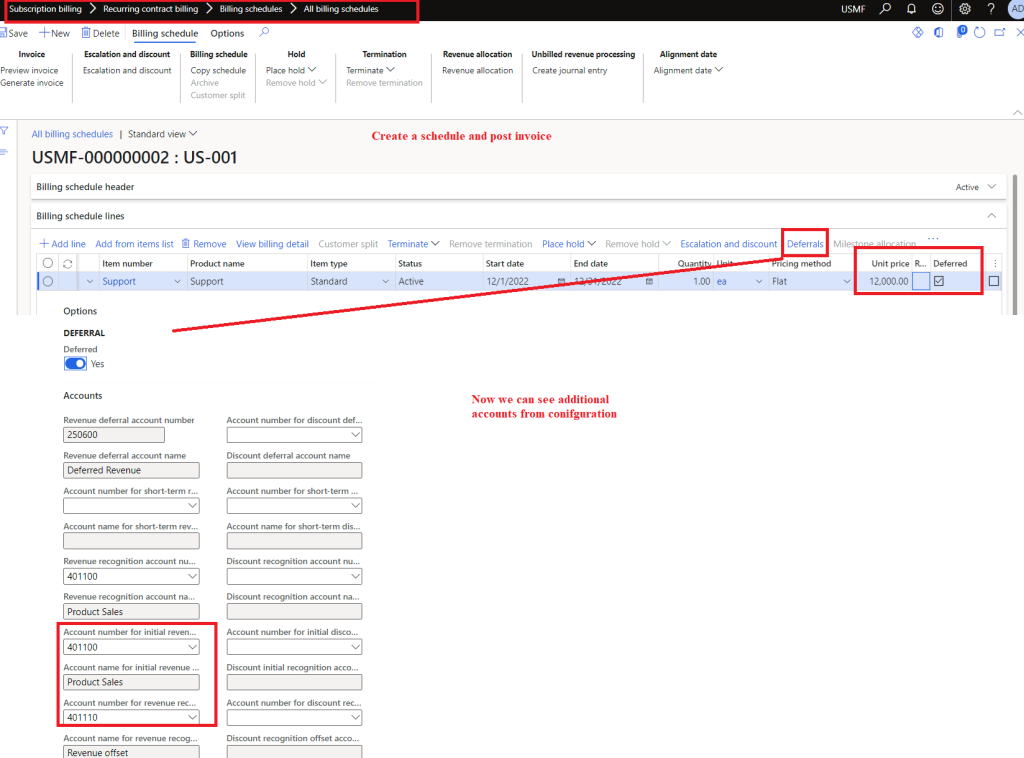

The Balance sheet method uses only two accounts. Therefore, less setup is involved. The Profit and loss method has two additional accounts, Initial recognition, and Recognition offset, for revenue, discounts, and costs, depending on the transaction type. These accounts are set up on the Deferral defaults page (Subscription billing > Revenue and expense deferrals > Setup). Although the example is focused on deferred revenue, the same concept can be applied to deferred discounts and deferred costs.

Reference : https://learn.microsoft.com/en-us/dynamics365/finance/accounts-receivable/deferral-posting-methods

Example

Sales invoice 1 has a total of $12,000 and has deferred revenue. The following tables show the distributions when this sales invoice is posted.

Balance sheet method

| Type | Account | Debit | Credit |

| Debit | Accounts receivable | 12,000.00 | |

| Credit | Deferred revenue | 12,000.00 |

Profit and loss method

| Type | Account | Debit | Credit |

| Debit | Accounts receivable | 12,000.00 | |

| Debit | Revenue recognition offset | 12,000.00 | |

| Credit | Deferred revenue | 12,000.00 | |

| Credit | Initial revenue recognition | 12,000.00 |

Sales invoice 2 has a total of $3,000 and doesn’t have deferred revenue.

| Type | Account | Amount |

| Debit | Accounts receivable | 3,000.00 |

| Credit | Revenue | 3,000.00 |

Balance sheet method totals for sales invoice 1 and 2 combined

| Account | Debit | Credit |

| Accounts receivable | 15,000.00 | |

| Revenue | 12,000.00 | |

| Deferred revenue | 3,000.00 |

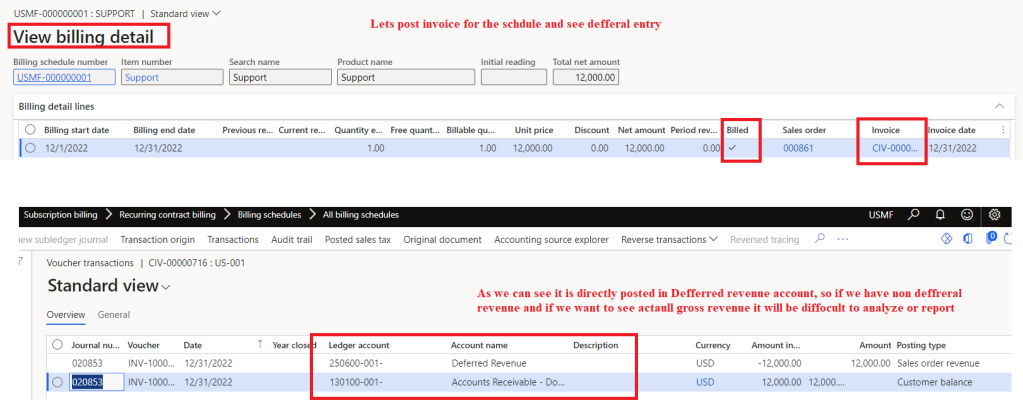

When the Balance sheet method is used, it isn’t as easy to see the gross revenue for a period. Some of the revenue is posted to the Deferred revenue account. Keep in mind that, as revenue is recognized each period, there are multiple debits and credits in the Deferred revenue account. Gross revenue for a given period will be mixed with the ins/outs of revenue recognition.

Profit and loss method totals for sales invoice 1 and 2 combined

| Account | Debit | Credit |

| Accounts receivable | 15,000.00 | |

| Revenue | 15,000.00 | |

| Revenue offset | 12,000.00 | |

| Deferred revenue | 12,000.00 |

All revenue goes to the profit and loss Revenue account. Then the deferred revenue is moved from the profit and loss statement to the balance sheet. You can easily see the gross revenue, because everything is posted to the Revenue account. However, some of that gross revenue is deferred. Therefore, it’s moved to the Deferred revenue account and recognized later.

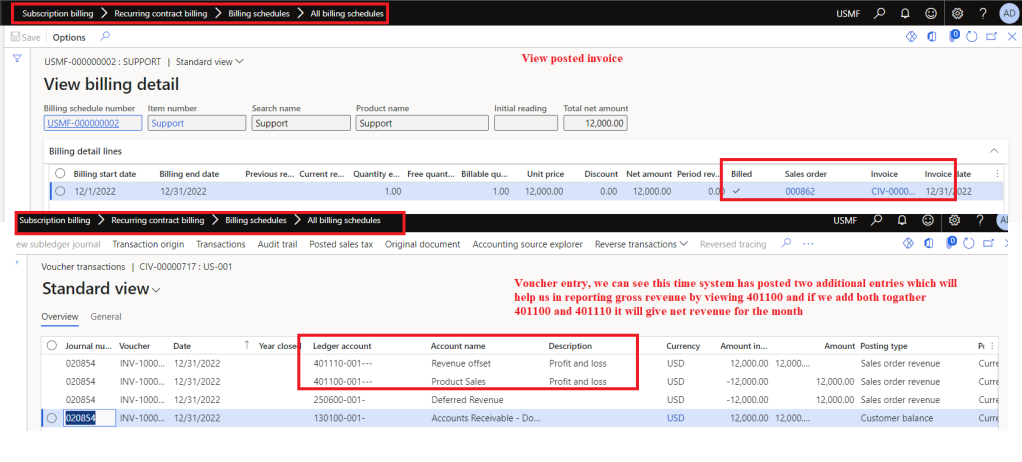

In the Profit and loss method, you can look at the Revenue account and Revenue offset account to see gross revenue of $15,000 and net revenue (net of deferred) of $3,000. Although the Profit and loss method can make reporting easier, there are more accounts to set up.

Lets see how it looks in Dynamics:

Balance sheet method:

Setup:

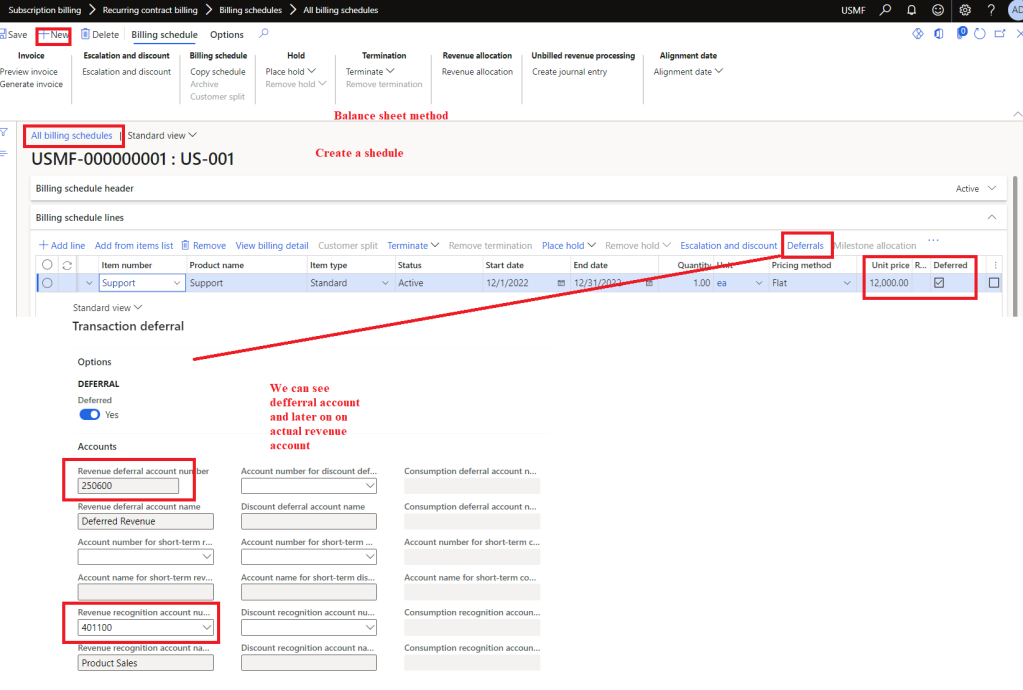

Create billing schedule or order with deferrals

Post invoice and view voucher

Profit and Loss method

Setup:

Create billing schedule or order with deferrals

Post invoice and view voucher

That’s it for this blog, hope this will help you to understand different methods for deferrals and accounting.

Thank you !!! Keep reading and sharing !!!

Thanks so much Mr. Saurabh Bharti

Will you give direct session also?

LikeLiked by 1 person

[…] are the previous blogs in this series: Part-1, Part-2, Part-3, Part-4, Part-5 and […]

LikeLike